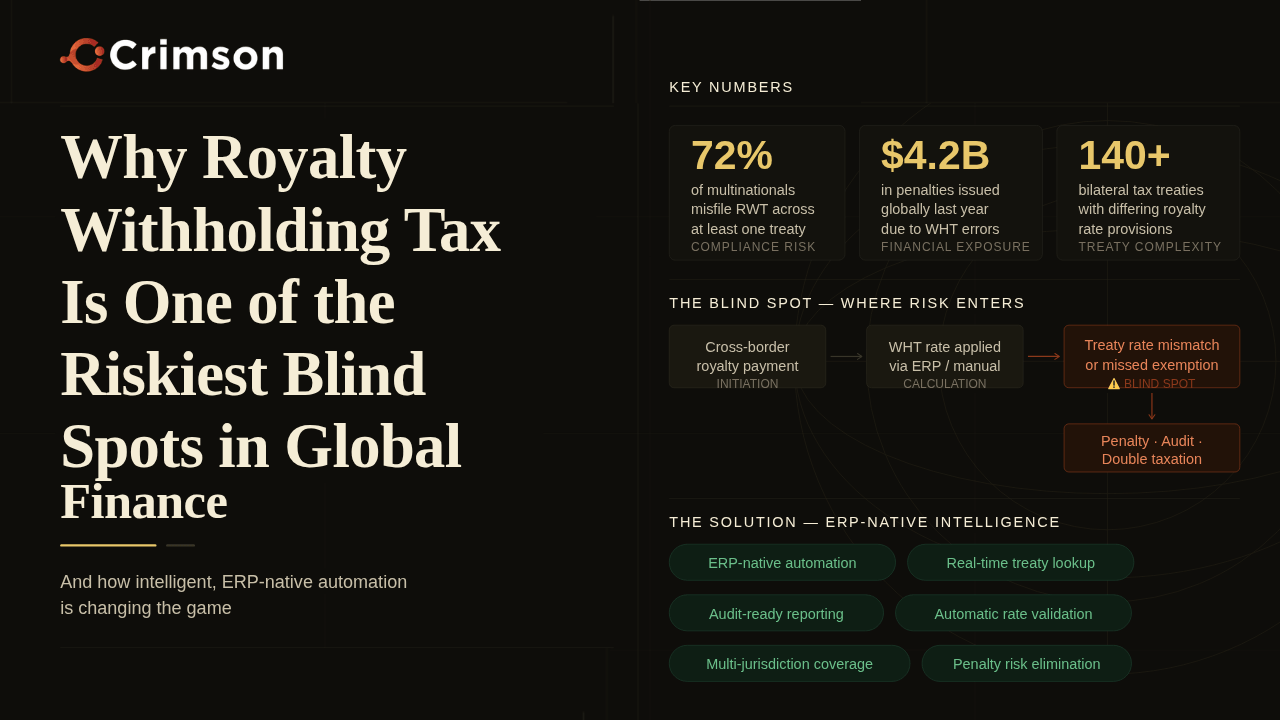

The Hidden Compliance Minefield

Every time a multinational makes a cross-border royalty payment — such as a patent license, software copyright, or exploitation of know-how — it steps into one of the most technically demanding areas of international tax. Withholding Tax (WHT) on royalties is not just a line on a remittance advice; it is a real-time compliance obligation that can expose a payer to penalties equal to 100% of the tax due, plus interest, if anything goes wrong.

Royalties carry a uniquely punishing twist: in most jurisdictions — including the UK under the ‘reasonable belief’ provisions of Section 911 ITA 2007 — payers can apply a reduced treaty rate at source without prior tax-authority approval. That flexibility sounds convenient, but it shifts the entire burden of proof onto the paying entity. If the documentation is incomplete, the classification is wrong, or a Tax Residency Certificate (TRC) has lapsed by a single day, the payer is liable. Not the vendor. Not the tax authority. The payer.

The global picture is made more complex by two competing treaty models. The OECD Model — favoured by developed nations — grants exclusive taxing rights to the Residence State, effectively resulting in 0% withholding at source, anchored in the Residence Principle. The UN Model, designed to protect developing economies, supports the Source Principle, allowing source jurisdictions to tax cross-border royalty payments at rates between 10–15%. For multinationals operating across dozens of jurisdictions, this means managing hundreds of unique rate-and-royalty-type combinations within double tax treaties, in real time, with zero margin for error.

“Just as minor customs errors can halt supply chains, a missing TRC or misclassified payment can freeze cross-border cash flows entirely.”

The stakes extend well beyond the tax department. WHT is critical for reconciling intercompany balances and avoiding secondary TP adjustments. Poor WHT execution does not just create a tax risk — it creates a cascading audit risk that can pull the board of directors into the frame for systemic compliance failures.

Where ERP Systems Fall Short

Most enterprise ERP systems were not built for the dynamic, double tax treaty-intensive nature of royalty WHT. Tax codes are static. TRC validity is not tracked automatically with relevant vendor outreach. And the critical difference between an Article 7 Business Profits payment (typically 0% WHT) and an Article 12 Royalty payment (taxable) is rarely determined by ERP logic — it requires contextual analysis of key data points such as GL code mappings and free-text line-item descriptions.

The consequences of this gap are well-documented: companies default to maximum statutory rates (often 20–30%) out of caution, trapping working capital in the source jurisdiction; historic reclaim windows expire unnoticed; and audit trails lack the “reasonable belief” justifications that regulators expect to see documented at the moment of execution — not reconstructed months later.

Offshore accounts-payable teams, however skilled, are rarely equipped to interpret double tax treaties in real time. The AP gap — between the volume of cross-border payments and the technical expertise required to classify each one correctly — is where WHT leakage quietly accumulates, often undetected until a tax authority enquiry forces a forensic review.

Crimson’s Answer: Deterministic Execution at the Point of Payment

Crimson’s WHT Management platform is built on a single premise: treaty compliance must be deterministic, not advisory. That means every payment is classified, validated, and documented before it leaves the ERP — not reconciled after the fact.

The platform operates as a SAP BTP-native, Clean Core extension, performing all treaty logic outside the ERP to eliminate custom ABAP code and technical debt. It covers four core capabilities:

- Bi-Temporal TRC Tracking: Certificates are validated against both the accrual and the clearing date, with automated vendor outreach triggered the moment a TRC approaches expiry.

- Multi-Factor Semantic Classification: A high-precision confidence-score matrix cross-references key data points such as GL and Line-item text to determine whether each payment falls under Article 7 or Article 12 — before the payment run.

- Deterministic Rate Application: Double tax treaty logic is applied at the point of payment, preventing both under-withholding (penalty exposure) and over-withholding (trapped cash).

- Automated Reclaim & Anomaly Resolution: Push-button resolution for historic reclaims, combined with real-time anomaly detection that surfaces upstream data errors before they becomeaudit findings.

The business case is direct. Crimson eliminates WHT leakage by preventing defaults to maximum statutory rates. It protects the P&L by preventing costly commercial ‘gross-ups’ triggered by missing TRCs. It mitigates audit risk by maintaining a complete, timestamped reasonable-belief audit trail for every transaction. And it provides the tax teams with a single, categorised source of cross-border royalty flow data — removing the manual ledger reconciliations that consume weeks of resource at year-end.

As tax authorities globally move toward real-time reporting, the window for manual, reactive compliance is closing. The question for finance and tax leaders is no longer whether to automate royalty WHT — it is how quickly they can move from static ERP logic to a deterministic, document-governed execution layer.

Crimson — Turning treaty complexity into deterministic execution.